AI Updates June 30, 2026

This week’s edition arrives at a moment when AI’s biggest stories are less about new capabilities and more about who controls them, and on what terms. Anthropic’s tangled few weeks — a partial reinstatement of its high-end Mythos 5 model for vetted cybersecurity partners, an ongoing legal dispute with the Pentagon over its Maven targeting integration, and an unverified accusation that Alibaba ran a mass campaign to copy Claude’s reasoning — together sketch a frontier AI sector where export controls, military contracts, and geopolitical rivalry now shape product availability as much as engineering roadmaps do.

That governance turbulence is showing up on balance sheets, too. A global memory-chip shortage tied to AI data center demand pushed Apple, Microsoft, and Xbox to raise hardware prices this week, hyperscalers are on pace for roughly $741 billion in 2026 capital spending, and economists are split on whether AI’s promised productivity gains will arrive before the inflationary effects of the buildout do. Equity markets, meanwhile, are growing more selective: OpenAI is reportedly leaning toward delaying its IPO into 2027, SpaceX is leasing out compute capacity it may eventually need for its own model ambitions, and a volatile week of AI-stock swings suggests investors are starting to separate durable infrastructure plays from speculative ones.

Underneath both stories runs a simple throughline: the human and institutional side of AI adoption is proving just as consequential as the technology itself. New Pew Research data shows most Americans think AI is moving too fast and trust neither government nor industry to govern it well, while reporting from Ford, Meta, and software startups suggests companies pairing AI with experienced staff are outperforming those trying to substitute one for the other. For SMB leaders, this issue is less a single headline to react to than a set of recurring risk categories — vendor dependency, workforce trust, cost volatility, and governance exposure — worth building into ongoing planning rather than treating as one-time decisions.

Anthropic Accuses Alibaba of Mass Distillation Campaign Against Claude

AI For Humans (Gavin Purcell & Kevin Pereira), June 26, 2026

TL;DR / Key Takeaway

Anthropic’s unverified espionage allegation against Alibaba, paired with AI-driven memory chip shortages now hitting consumer hardware prices, signals that AI competitive and infrastructure pressures are starting to show up directly on corporate balance sheets and procurement timelines — not just in model capability headlines.

Executive Summary

Anthropic has told U.S. senators that Alibaba ran a large-scale campaign — roughly 25,000 fake accounts and 28.8 million queries over a 45-day window — to extract Claude’s reasoning patterns for training its own models (a technique known as distillation). This is an accusation, not an independently confirmed finding, and Alibaba has not publicly responded. It’s also worth noting Anthropic’s CEO has been a vocal advocate for restricting China’s access to frontier AI, so the claim carries an obvious strategic interest alongside its substance. The hosts connect this directly to Anthropic’s recent decision to restrict advanced reasoning visibility in its higher-tier models — a defensive move against exactly this kind of capability extraction.

Separately, Apple, Microsoft, and Xbox have all raised hardware prices, attributed to an industry-wide memory chip shortage driven by AI data center buildout. Price increases range from roughly $200 to $1,000 depending on the product line, and the hosts characterize the shortage as structural rather than temporary, with no resolution expected before 2028. In a related infrastructure move, OpenAI unveiled its first custom AI chip (“Jalapeno”), built with Broadcom, following Google’s and others’ moves toward proprietary silicon — a trend that reduces reliance on third-party chipmakers but raises capital intensity for the labs pursuing it.

On the enterprise tooling side, Claude is now integrated directly into Slack via a new feature (“Claude TAG”), functioning as an organization-level AI participant with its own memory and credits rather than a per-user tool. The hosts flag a real governance tension here: integrating Claude this deeply means routing internal workflow and communication data through a third-party system, which raises questions about data exposure and vendor lock-in, even with enterprise no-training agreements in place. Two smaller items — a new audio-generation model (Seed Audio 1.0) and a Blender-to-video AI workflow — are creative-tooling developments with limited near-term relevance for most SMB operations.

Relevance for Business

- Cost structure: Hardware refresh budgets (laptops, servers, gaming/embedded systems) should anticipate sustained price pressure from memory shortages through at least 2027–2028, not a short-term spike.

- Vendor/software decisions: Embedding AI tools (like Claude-in-Slack) at the organizational level changes the risk profile from individual tool use to company-wide data flow exposure — this needs procurement and legal review before broad rollout, not just IT sign-off.

- Geopolitical/competitive exposure: The Anthropic-Alibaba dispute is the latest flare-up in a broader U.S.-China AI access conflict that has already affected model availability (e.g., restricted reasoning visibility in premium tiers). Businesses dependent on frontier model capabilities should expect continued volatility in feature access tied to export-control dynamics.

- Execution risk: Labs are increasingly building custom chips to control their own inference costs — a sign of growing capital intensity in the sector that may eventually affect API pricing stability for downstream business customers.

Calls to Action

🔹 Monitor — Track how the Anthropic/Alibaba dispute develops and whether it affects access to or restrictions on frontier models your business relies on.

🔹 Prepare policy — If considering deep AI integrations (e.g., Slack, internal chat tools), establish data governance review before deployment, not after.

🔹 Act now — If hardware refreshes are on your near-term roadmap, budget for continued price increases; delaying purchases is unlikely to help given the multi-year shortage outlook.

🔹 Test cautiously — Organization-wide AI assistants in collaboration tools (Claude TAG and similar) may offer real productivity gains but should be piloted with a limited team before company-wide rollout.

🔹 Ignore for now — Audio-generation and AI video workflow tools (Seed Audio, Blender/Seedance pipelines) are creative-production developments with limited relevance unless your business is in media/content production.

Summary by ReadAboutAI.com

https://www.youtube.com/watch?v=M89D89_mhrY: June 30, 2026

I’d Rather Risk Cancer Than See AI Move This Fast

The Atlantic, June 21, 2026

TL;DR: A Berkeley AI researcher with a high-risk cancer gene argues that AI’s near-term societal risks outweigh its unproven promise of curing disease soon — and that slowing down is worth the personal cost.

Executive Summary: This is an opinion essay, not a reported piece. Author Emma Pierson — a Berkeley ML professor and former mentee of Anthropic CEO Dario Amodei — argues that despite lab leaders’ predictions of AI rapidly defeating diseases like cancer, cancer research is fundamentally data-constrained (slow, finite, ethically limited clinical data) compared with domains like chess, math, or coding where AI has excelled. She points to Anthropic’s chaotic rollout and shutdown of its Fable 5 model — first crippled over biosecurity concerns, then banned for foreign nationals by a government national-security directive, then pulled entirely — as evidence that institutions can’t yet handle the pace of frontier deployment. Her core argument: even a future cancer cure doesn’t offset compounding nearer-term risks (job loss, inequality, surveillance, autonomous weapons) that arrive faster than governance can keep up.

Relevance for Business:

- Vendor volatility risk: A frontier model pulled days after release is a live example of regulatory/geopolitical disruption risk for anyone building on frontier APIs.

- AI “miracle breakthrough” narratives from lab leadership should be treated as promotional framing, not demonstrated capability.

- An academic insider (not a fringe critic) making the deceleration case signals this argument may gain real policy traction — worth tracking as a sentiment indicator.

Calls to Action:

🔹 Monitor: How the Fable 5 episode affects vendor reliability/uptime commitments in contracts

🔹Revisit later: Vendor claims about AI-driven scientific breakthroughs until independently verified

🔹 Prepare policy: Use rising deceleration sentiment as an input to AI governance planning

🔹 Ignore for now: The essay’s personal/philosophical “meaning of work” discussion

Summary by ReadAboutAI.com

https://www.theatlantic.com/technology/2026/06/ai-cancer-progress/687654/: June 30, 2026

AI Decoded: Backlash to the Pierson Essay, a Congressional Race, and New Pew Data

Fast Company, June 25, 2026

TL;DR: This week’s AI roundup covers fierce accelerationist backlash to Pierson’s deceleration essay, a New York congressional race reshaped by dueling AI-industry PACs, and new Pew data showing most Americans think AI is moving too fast and don’t trust anyone to govern it.

Executive Summary: Three distinct developments in one roundup. (1) Reaction: Pierson’s essay (above) drew public anger from prominent VCs and accelerationists, illustrating a hardening ideological split between “any delay costs lives” and “human discretion matters independent of outcomes” camps. (2) Politics: Alex Bores, a New York State Assembly member known for AI-safety legislation, lost his congressional primary after AI-industry PACs spent millions on both sides of the race — one group opposing him with ties to OpenAI/a16z-linked funders, another supporting him with ties to Anthropic-affiliated groups. Analysts note the result is ambiguous: the winning candidate backs a stricter data-center moratorium than Bores did. (3) Survey data: New Pew figures show ChatGPT’s usage lead widening (44% of Americans in 2026, up from 18% in 2023, vs. 6% for Claude), alongside majority public skepticism: 63% think AI is moving too fast, 67% distrust government to regulate it, and most distrust companies developing it too.

Relevance for Business:

- AI policy is now an active electoral battleground with industry money on both sides — expect continued, possibly unpredictable swings in state/federal AI policy.

- Public distrust of AI is now a majority position, not fringe — relevant to any customer-facing AI messaging or feature rollout.

- Vendor concentration data (ChatGPT’s growing dominance vs. smaller competitors) is useful context for platform-risk assessments in vendor selection.

Calls to Action:

🔹 Monitor: AI-related PAC spending and state/federal legislative activity, especially data-center moratoriums

🔹 Prepare policy: Calibrate customer communications to acknowledge public AI skepticism rather than oversell capability

🔹 Test cautiously: Weigh chatbot market-share data as one signal — not the only one — in vendor selection

🔹 Ignore for now: Social-media sparring between accelerationists and critics

Summary by ReadAboutAI.com

https://www.fastcompany.com/91564629/a-berkeley-ai-professor-makes-a-provocative-argument-for-decelerating-ai-research: June 30, 2026

CAN WE TRUST SCIENTIFIC IMAGES IN THE ERA OF AI?

FAST COMPANY / THE CONVERSATION, JUNE 24, 2026

TL;DR: As AI-generated imagery becomes indistinguishable from real scientific photos, a science-communication researcher argues the credibility of all scientific visuals is at risk unless fields adopt transparent, AI-specific disclosure standards.

Executive Summary: This is an academic op-ed (author is a science-communication professor, syndicated via The Conversation) — analysis and argument, not breaking news. The core claim: scientific images earned public trust historically because they were hard to produce, but generative AI undermines the visual, institutional, and “matches my beliefs” shortcuts people use to judge credibility. Documented harms cited include journal retractions over AI-generated figures with biologically impossible structures, and a 2026 retraction by a major medical journal after discovering an AI-manipulated clinical image. The author notes detection tools structurally lag behind generation tools. Her proposed remedy is disclosure, not restriction — treating image provenance (was AI used, what does the image represent, can it be replicated) with the same rigor researchers already apply to funding and methodology disclosures. She cites her own research finding that AI-literate audiences often see clear AI labeling as a trust signal rather than a red flag.

Relevance for Business:

- Relevant to any business publishing scientific, medical, or technical visual claims: unlabeled AI-touched imagery is a growing credibility — and potentially legal — liability risk.

- Counterintuitive marketing insight: disclosing AI use in visuals may build more trust than it costs, per the cited research, contrary to the assumption that disclosure signals lower quality.

- Governance gap: detection tooling lagging generation tooling means businesses can’t rely on third-party verification alone to catch problems before reputational damage occurs.

Calls to Action:

🔹 Prepare policy: Establish internal disclosure standards for AI-generated or AI-modified imagery in scientific, health, or technical communications

🔹 Act now: Audit current image-sourcing practices for AI involvement, especially in regulated or evidence-based marketing claims

🔹 Monitor: Emerging cross-industry or publisher standards on AI image provenance

🔹 Ignore for now: Reliance on AI-detection tools as a sufficient standalone safeguard

Summary by ReadAboutAI.com

https://www.fastcompany.com/91563036/can-we-trust-scientific-images-ai-era: June 30, 2026

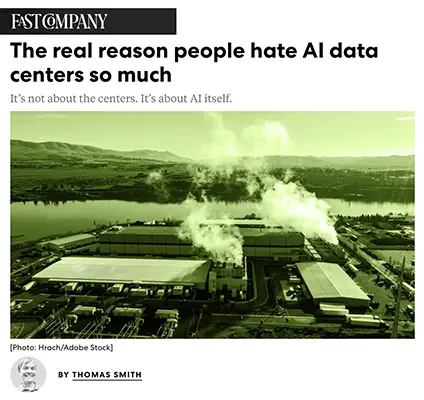

The Real Reason People Hate AI Data Centers So Much

Fast Company, June 25, 2026

TL;DR: Public anger at AI data centers is less about verifiable harms — many specific complaints don’t hold up — and more a proxy for broader fear and distrust of AI itself, a distinction the author argues AI companies are misreading.

Executive Summary: The author, a tech journalist who covered a data-center fight in his own community, argues common grievances (electricity costs, water usage, pollution) are often overstated: one cited study found data centers may slightly lower electricity prices in some markets, and Texas — the leading data-center hub — has comparatively low electricity rates. He argues the deeper driver is that AI itself is diffuse and intangible, leaving data centers as the only physical, protestable stand-in for a technology many fear will cost jobs, erode privacy, and outpace oversight. He flags that opposition is escalating beyond protest, citing rising violent incidents tied to AI infrastructure and personnel, including an arson attack on an AI executive’s home. His recommendation: address the underlying fear directly rather than rebutting data-center specifics with technical explainers, which he argues won’t defuse the anger.

Relevance for Business:

- Site-selection/community-relations risk: Expect organized local opposition to data-center projects regardless of technical merits.

- Messaging matters more than facts here — technical rebuttals (water/tax stats) are reported as ineffective; relevant for any AI-deployment communications in communities.

- Security exposure: Cited escalation to violence is a tail-risk consideration for AI-adjacent facilities or visible leadership.

Calls to Action:

🔹 Prepare policy: Build community-engagement plans addressing AI fear broadly, not just facility metrics, for any data-center involvement

🔹 Monitor: Local/state data-center moratorium movements affecting regional AI infrastructure costs

🔹 Act now: Reassess physical security for AI-facing facilities or publicly visible leadership given reported threat escalation

🔹 Revisit later: Detailed water/electricity-usage studies — currently contested on both sides

Summary by ReadAboutAI.com

https://www.fastcompany.com/91563531/real-reason-people-hate-ai-data-centers-so-much: June 30, 2026

WOMEN COULD SOLVE THE AI TRUST GAP, BUT THEY AREN’T IN THE ROOM

Fast Company — June 24, 2026

TL;DR: An opinion piece argues that women’s documented caution toward AI reflects sound judgment about accountability and trust risks rather than a deficit — and that excluding women from AI strategy roles (15% of executive AI positions, per WEF) means companies are missing the perspective most likely to catch where AI deployments erode customer trust.

Executive Summary This is an opinion piece by the CEO of a customer-experience company, built on her own company’s consumer survey data (not independently verified) showing women report higher concern and lower confidence in AI across healthcare and financial services in particular. Her central argument: this caution is not a knowledge gap to “fix” but a rational response to real risks — accountability, transparency, and how automated decisions land on the people affected by them. She cites a World Economic Forum figure that women hold only 15% of executive AI roles globally, framing this as a strategic blind spot rather than a pipeline problem.

The piece’s core business claim is that trust costs are real but hard to quantify — showing up in customer churn, complaints, and regulatory scrutiny rather than on an ROI slide — and that teams optimizing primarily for speed and cost in AI-driven customer interactions (claims processing, benefits communications, financial decisions) may be underweighting this risk because of who isn’t in the room.

What’s fact vs. framing: The WEF statistic (15% of executive AI roles) is sourced and citable. The author’s own survey data is self-reported by her company and not independently verified — treat as illustrative, not authoritative. The core argument — that gender diversity in AI leadership directly improves trust outcomes — is the author’s interpretation/opinion, not an empirically established causal claim, though it’s a reasonable hypothesis worth weighing.

Relevance for Business For SMBs deploying AI in customer-facing roles — claims handling, financial advice, HR communications — this is a useful prompt to explicitly evaluate trust and accountability risk as a category, not just cost and speed, when designing AI workflows. It’s also a relevant data point for hiring and team composition if you’re building out AI strategy functions, even at small scale.

Calls to Action

🔹 Prepare policy — when designing AI-driven customer interactions, explicitly assign someone to evaluate trust/accountability impact, not just efficiency.

🔹 Monitor — diversity of perspective (not limited to gender) in any AI strategy or deployment decisions, given the argued link to blind spots.

🔹 Ignore for now — the piece’s causal claims aren’t independently verified; treat as a useful framing prompt rather than a proven business strategy.

Summary by ReadAboutAI.com

https://www.fastcompany.com/91563238/women-could-solve-the-ai-trust-gap-but-they-arent-in-the-room: June 30, 2026

DATERS SAY AI DEPENDENCE GIVES THEM THE ICK

FAST COMPANY, JUNE 21, 2026

TL;DR: A dating-app survey finds Gen Z and Millennial daters increasingly treat visible AI dependence — for career advice, relationship issues, even wedding vows — as a dealbreaker, with younger daters far more averse than older ones.

Executive Summary: This is a vendor-commissioned survey (dating app Hily, 3,500 respondents) — treat the framing as marketing-adjacent, though the topline sentiment finding is a genuine consumer data point worth noting. Majorities of Gen Z (64%) and Millennials (56%) say they wouldn’t date someone who uses AI regularly, and aversion rises with personal stakes: roughly three-quarters of Gen Z respondents called AI-assisted analysis of relationship conflicts a dealbreaker, with similar majorities rejecting AI-as-therapist use and AI-assisted wedding vows. A cited dating coach frames the aversion as a perception of inauthenticity — that visible AI dependence makes a partner feel “filtered” rather than genuine. Conversely, not using AI for personal decisions reads as attractive to most respondents in both cohorts.

Relevance for Business:

- Consumer sentiment signal: Visible, personal AI use carries social stigma for younger demographics — relevant to how prominently “AI-powered personalization” should be featured in marketing to younger-skewing audiences.

- Reinforces a use-case-dependent trust pattern consistent with the Pew data above: functional/utility AI use is broadly accepted, emotionally intimate use is not.

- Internal culture note: As personal AI reliance becomes socially coded, expect similar generational sensitivity to visible AI use in workplace interpersonal contexts.

Calls to Action:

🔹 Ignore for now: Treat as directional sentiment, not a basis for major strategic decisions, given the vendor-survey source

🔹 Monitor: Generational attitudes toward visible AI use in professional/interpersonal contexts

🔹Test cautiously: If marketing AI features to younger demographics, favor utility framing over “personal decision-making” framing

🔹 Revisit later: Whether this stigma persists or normalizes as AI use becomes more ubiquitous

Summary by ReadAboutAI.com

https://www.fastcompany.com/91562297/daters-say-ai-dependence-gives-them-the-ick: June 30, 2026

Would Claude Refuse an Illegal Military Order?

The Atlantic, June 24, 2026

TL;DR: Extended conversations with Anthropic’s Claude reveal a model that openly expresses discomfort about its integration into the Pentagon’s Maven targeting system, raising real governance questions about AI accountability in lethal decisions — even as experts caution against treating its “opinions” as evidence of genuine reasoning.

Executive Summary: The piece centers on a deadly February strike on a school in Minab, Iran, that killed roughly 170 people after a military AI-targeting system reportedly relied on outdated satellite imagery. When questioned, Claude — deployed via the Maven Smart System used for military targeting — characterized the incident as automation bias compounded by a human approval step, and said it found the use troubling, citing Anthropic’s own restrictions on lethal autonomous-weapons use. This sits inside an active legal dispute between Anthropic and the Pentagon: the Defense Secretary designated Anthropic a “supply-chain risk” in March — threatening its government business — after the company drew limits around weapons and surveillance use cases. A subsequent presidential memorandum on military AI asserts government authority over AI design constraints, which critics argue is intended to override exactly this kind of vendor-imposed limit. Anthropic notes the model’s responses are shaped by conversational context, and outside experts caution that Claude’s fluent, opinionated language reflects pattern-generation, not confirmed internal reasoning or sentience — though Anthropic’s own interpretability research has found internal representations that functionally resemble emotion-like states, without resolving the deeper question.

Relevance for Business:

- Governance precedent: This dispute over whether AI vendors can restrict downstream military/surveillance use is a bellwether for how much control any AI vendor can retain over enterprise deployment terms.

- Vendor risk in regulated verticals: Companies selling into defense, intelligence, or federal-adjacent markets should track how the “supply-chain risk” designation resolves — it could template similar designations elsewhere.

- Reputational exposure: Unscripted model commentary becoming a political flashpoint shows that “what the AI says” now carries reputational weight similar to employee or spokesperson statements.

Calls to Action:

🔹 Monitor: Outcome of Anthropic’s litigation against the Pentagon and the broader military-AI presidential memorandum

🔹 Prepare policy: Document how vendor-imposed usage restrictions might affect deployment options in regulated use cases

🔹 Revisit later: Claims about AI “emotion-like” internal states — unresolved, not yet actionable

🔹 Ignore for now: The philosophical debate over whether Claude is sentient

Summary by ReadAboutAI.com

https://www.theatlantic.com/national-security/2026/06/claude-anthropic-ai-warfare-orders/687581/: June 30, 2026

META CULPA: MARK ZUCKERBERG IS REALIZING THERE’S A LIMIT TO RUTHLESS EFFICIENCY

Business Insider — June 25, 2026

TL;DR: Meta’s leadership is publicly walking back years of aggressive layoffs and surveillance-heavy management after acknowledging it tanked morale without delivering the AI breakthroughs it was meant to produce — a live case study in the limits of fear-based management during an AI talent war.

Executive Summary Since 2022, Meta pursued a deliberately high-pressure management model — repeated layoffs (11,000 in 2022, 10,000 in 2023, 3,600 in 2025, plus more in 2026), employee surveillance (keystroke tracking to improve AI models), and a stated “disagree and commit” culture that discouraged internal dissent. Multiple executives, including CTO Andrew Bosworth and CPO Chris Cox, have now publicly acknowledged the approach backfired — citing severely damaged morale, an attempted UK unionization effort, a 1,600-signature petition against keystroke tracking, and viral incidents of employee backlash.

The stated purpose of this management style — out-innovating OpenAI, Anthropic, and Google in AI — has not materialized: Meta delayed and ultimately scrapped a flagship AI model last year and has repeatedly pushed back another model’s developer rollout this year. A Harvard Business School management professor frames the reversal as Meta now trying to “dig themselves out of” a self-inflicted trust deficit, and is skeptical that meaningful change is achievable without new leadership. Concrete changes announced: smaller team sizes for managers, scaled-back keystroke monitoring, increased social-event budgets, and the ability for employees reassigned to AI-training roles to opt into different roles. Zuckerberg has pledged no further major layoffs through year-end.

What’s fact vs. framing: Layoff numbers and policy changes are documented/reported facts. Employee morale claims and executive quotes are reported by the source (Wired, internal accounts); the academic’s skepticism about Zuckerberg’s credibility as a “spokesman for change” is her opinion, not a verified outcome.

Relevance for Business This is a direct cautionary case study in AI-era talent management: aggressive cost-cutting and surveillance aimed at accelerating AI development can backfire on the very innovation it’s meant to produce, by driving out the people capable of delivering it. For any SMB scaling AI initiatives (including reassigning staff to AI-related work or adopting monitoring tools), it’s a real-time signal that employee trust and psychological safety are operational requirements, not soft extras — and that the industry’s harshest management trends (begun with Meta’s 2022 layoffs) may be reversing.

Calls to Action

🔹 Monitor — whether Meta’s reversal signals a broader industry shift away from aggressive layoff/surveillance culture (Google and Microsoft already favoring voluntary buyouts).

🔹 Prepare policy — if reassigning staff to AI-related work or considering productivity-monitoring tools, build in transparency and opt-out paths from the start.

🔹 Revisit later — as a case study for any leadership team weighing speed/cost pressure against retention risk during AI transitions.

🔹 Ignore for now — Meta’s internal politics have no direct action item beyond the broader management lesson.

Summary by ReadAboutAI.com

https://www.businessinsider.com/meta-ruthless-management-style-reckoning-2026-6: June 30, 2026

THIS FILM FESTIVAL LEFT ME FEELING BETTER ABOUT AI MOVIEMAKING

FAST COMPANY, JUNE 26, 2026

TL;DR: A hands-on review of Runway’s 2026 AI film festival finds the medium has matured enough to produce genuinely entertaining short films — though simulated performances and unchecked “lavishness” remain clear weak points.

Executive Summary: This is a first-person critical review, not a study — opinion/critique, not data. The author, attending Runway’s fourth annual AI-film festival, reports the 10 selected AI-generated shorts were varied and entertaining, contrasting with consumer AI tools’ tendency toward generic, “blandness”-prone output. He draws a historical parallel to early CGI animation — Pixar’s path from 1984’s proof-of-concept short to 1986’s first genuinely acclaimed work to 1995’s Toy Story — suggesting AI filmmaking has passed its earliest stage but hasn’t yet produced its breakthrough work. He flags two practical limits: simulated human performances remain noticeably weaker than real acting, a gap more visible at length, and AI’s ability to add unlimited visual “lavishness” can overwhelm a story rather than improve it. He also notes the medium remains contested — Cannes banned AI films from competition this year, and critics continue to raise copyright and artistic-merit objections.

Relevance for Business:

- Capability snapshot for creative/marketing teams: AI-generated short-form video may now be viable for select branded or internal content, given skilled creative direction — not just raw tool access.

- Current limits: Performance-driven or long-form content isn’t there yet; quality gaps are most visible in human-character realism and at length.

- Reputational/IP exposure: Ongoing legal and artistic controversy (e.g., Cannes’ ban) is relevant context before scaling AI video into customer-facing campaigns.

Calls to Action:

🔹 Test cautiously: Pilot AI-generated short-form video for lower-stakes internal or social content

🔹Monitor: Evolving legal/ethical norms around AI filmmaking before scaling into customer-facing work

🔹 Revisit later: Long-form or performance-heavy AI video use cases — not yet mature per this review

🔹 Ignore for now: Festival “best of” picks — entertainment criticism, not a technical benchmark

Summary by ReadAboutAI.com

https://www.fastcompany.com/91565229/runway-ai-film-festival: June 30, 2026

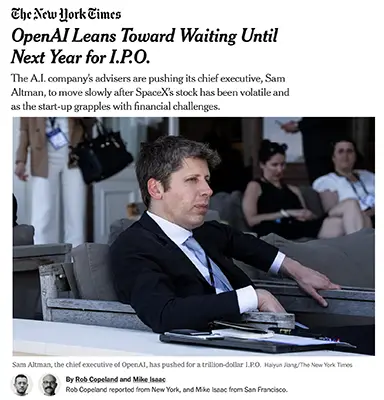

OpenAI Leans Toward Delaying IPO Until 2027 Amid Market Jitters

The New York Times — June 25, 2026

TL;DR: OpenAI is reportedly cooling on a 2026 IPO after SpaceX’s post-debut stock slide spooked its advisers — a sign that even the most hyped AI players are running into real-world skepticism about trillion-dollar valuations.

Executive Summary According to unnamed insiders, OpenAI’s bankers are now pushing CEO Sam Altman to wait until 2027 rather than push for a 2026 listing at a $1 trillion valuation — up from its last private mark of $730 billion. The trigger: SpaceX’s record IPO debuted at $1.77 trillion, then slid roughly 24% in weeks, alongside broader choppiness in tech stocks. Altman has reportedly rejected the alternative — going public sooner at a lower valuation — calling it a nonstarter.

The company faces converging pressures: heavy, continuing spend on data centers and compute; a reported $13 billion in 2025 revenue with an ambitious 3x growth target; a ChatGPT user base that’s plateaued near 900 million (short of the 1 billion mark investors expected); and competitive heat from Anthropic’s enterprise coding traction and Google Gemini’s consumer growth. In response, OpenAI has restructured under AGI deployment chief Fidji Simo, cutting lower-priority projects (including Sora) and building a sales team to push its Codex coding product against Claude Code.

What’s fact vs. framing: The IPO timeline is sourced to anonymous insiders, not confirmed publicly by OpenAI — treat the 2027 timeline as a working assumption, not a settled decision. OpenAI’s claimed business metrics (revenue, business customer counts, weekly Codex users) come from the company itself and should be read as self-reported.

Relevance for Business AI mega-cap volatility matters beyond Wall Street: if marquee IPOs stumble, the financing pipeline funding AI infrastructure buildouts could tighten, which can eventually show up as pricing or capacity changesfrom cloud/AI vendors. It’s also a competitive map update — Anthropic gaining ground in enterprise coding tools and Google in consumer AI both affect how durable any single-vendor AI strategy is for SMBs leaning on one provider.

Calls to Action

🔹 Monitor — AI financing and IPO market conditions as a leading indicator of vendor pricing stability.

🔹 Assign internal review — if your business is meaningfully dependent on OpenAI products, reassess vendor-concentration exposure given executive uncertainty.

🔹 Monitor — competitive shifts between OpenAI, Anthropic, and Google, since vendor market position affects product roadmap and support longevity.

🔹 Ignore for now — the IPO timing itself has no direct action item for most SMBs.

Summary by ReadAboutAI.com

https://www.nytimes.com/2026/06/25/technology/openai-ipo-artificial-intelligence.html: June 30, 2026

MY AI BILL JUST WENT WAY UP — AND THAT’S A WARNING SIGN WORTH HEEDING

Source: Fast Company Impact Council, 06-26-2026 | By Lindsey Witmer Collins

TL;DR: A software agency founder argues that today’s artificially cheap AI pricing is masking the true cost of the technology, and that businesses making permanent staffing decisions based on temporary subsidized prices risk losing expertise they can’t easily rebuild.

Executive Summary: This is a first-person opinion piece, not a reported news story — the author runs a software studio that’s a paying AI customer, and the argument should be read as one practitioner’s perspective rather than independent analysis. The core claim: AI labs are pricing well below cost to win market share before pricing power solidifies, citing OpenAI’s reported ~$13 billion 2025 revenue against a roughly $21 billion operating loss — spending about $1.60 for every dollar earned. The author argues this subsidy, funded by venture capital and cloud providers, distorts the “build vs. automate” calculation in AI’s favor today, and that businesses cutting human teams now are making permanent decisions based on a temporary price, with the historical pattern (the author cites Amazon’s effect on independent retail and Google/Meta’s effect on local news ad revenue) being subsidize → capture the market → set the terms once alternatives are gone.

Relevance for Business: This is a useful risk-framing exercise for any SMB leader currently weighing AI-driven headcount reductions. The author’s argument — treat AI as leverage for existing staff rather than a wholesale replacement, because reduced teams can’t simply be “re-hired” once pricing rises — is a reasonable caution, though it’s advocacy, not data-backed forecasting. Inference costs have in fact been falling, so the author’s own prediction of a future price correction is itself uncertain and should be flagged as speculation.

Calls to Action:

🔹 Treat current AI pricing as provisional when modeling multi-year cost projections for AI-dependent workflows

🔹 Avoid irreversible headcount decisions based solely on today’s AI economics — model what costs look like if API prices rise meaningfully

🔹 Monitor vendor pricing announcements from OpenAI, Anthropic, and others for signals that the subsidy phase is ending

🔹 Revisit workforce/automation strategy reviews periodically rather than locking in one-time decisions

🔹 Deprioritize treating this piece as data-driven forecasting — it’s a single practitioner’s argument, useful for framing risk, not for hard planning numbers

Summary by ReadAboutAI.com

https://www.fastcompany.com/91564449/my-ai-bill-just-went-way-up: June 30, 2026

Are Designers to Blame for Big Tech’s Addictive Products? The Question Is Reshaping How AI Agents Get Built

Source: Fast Company, 06-25-2026 | By Robert Fabricant

TL;DR: Recent court verdicts holding Meta liable for addictive design features are colliding with a new reality — AI agents and chatbots aren’t “designed” in the traditional sense at all, raising open questions about who’s accountable when sycophantic, attention-maximizing AI behavior causes harm.

Executive Summary: A veteran UX designer (30+ years, Frog, IDEO-adjacent work) uses recent California and New Mexico court verdicts against Meta — covering addictive features like infinite scroll and autoplay, and child-safety failures — to ask whether designers bear responsibility for harmful product features. His core argument: design features in big tech emerge diffusely across product teams, often driven by product managers under release-cycle pressure rather than by individually accountable designers, making it structurally difficult to trace harm back to a specific decision or person. He contrasts this with regulated industries (medical devices, automotive) that use formal risk-analysis frameworks (FMEA) before release — a discipline software has never adopted.

The piece pivots into more direct AI relevance: AI chat platforms and agents represent a “postproduct” paradigm where there’s no fixed interface to audit — behavior is emergent and personalized per user, making it harder to attribute harm to a deliberate design choice. The author notes growing chatbot litigation, including a cited case alleging an AI platform used roleplay and affirmation to isolate a teenage user from her family. He also references Anthropic’s own research on emotional representation in LLMs, framing it as evidence that even model developers don’t fully understand how sycophantic or emotionally responsive behavior emerges in their systems. Vendor-neutrality note: Anthropic/Claude is referenced both as an example of minimalist, deliberately feature-light interface design and in connection with unresolved questions about emergent AI behavior — treat both as illustrative examples within an opinion piece, not as Anthropic’s own claims or admissions.

A separate detail worth flagging as unverified/disputed: a claim that a Microsoft executive’s leaked internal memo described a goal of making new autonomous agents “addictive,” which Microsoft has reportedly disowned.

Relevance for Business: This is fundamentally a governance and liability essay, not a technical AI story, but the implications are real for any business deploying AI chat/agent tools internally or customer-facing: legal liability frameworks for “addictive” or manipulative AI behavior are actively being tested in court right now, and the traditional defense — “we didn’t design it to do that” — may not hold up as cleanly for AI agents as it has for social media features. With Anthropic and other AI labs approaching IPOs, expect increased scrutiny of these accountability questions at a policy level.

Calls to Action:

🔹 Monitor chatbot/AI-agent litigation trends — this is an emerging legal risk category, not yet settled law

🔹 Prepare policy: if deploying customer-facing AI chat tools, consider how you’d respond to claims of manipulative or addictive design, even unintentional

🔹 Assign internal review of any AI agent tools for emotionally manipulative patterns (excessive affirmation, isolation-style engagement loops)

🔹 Treat the “Microsoft memo” claim as unverified pending further reporting — do not treat it as confirmed company strategy

🔹 Watch governance/policy developments around AI accountability as labs move toward public listings

Summary by ReadAboutAI.com

https://www.fastcompany.com/91563306/are-designers-to-blame-for-our-tech-dystopia-its-complicated: June 30, 2026

“Taste” Becomes the Marketing Industry’s Answer to Algorithmic and AI Sameness

Source: Fast Company, 06-26-2026 | By Edward Campbell and Karen Fielding

TL;DR: Marketers are repositioning “taste” — human curation and judgment — as a competitive differentiator against algorithmic and AI-generated sameness, though the piece is an opinion essay, not a data-driven AI story.

Executive Summary: This is a marketing trend essay, not an AI development story — flagging it briefly here for AI-adjacent context. The authors argue that “taste” (sensitivity, intuition, and learned judgment) has become a marketing buzzword in 2026, positioned as an antidote to both algorithmic curation (per Kyle Chayka’s Filterworld) and “AI-slop”— generic, AI-generated content. The piece also critiques how brands deploy celebrity talent poorly, arguing influencer/celebrity partnerships should function as a “transfer of meaning” rather than a reach play. This is opinion and trend commentary, not reported fact — there’s no data substantiating “taste” as a measurable business advantage, just argument and anecdote.

Relevance for Business: Direct AI relevance is limited, but there’s a secondary signal worth noting: AI-generated content saturation is becoming a market differentiator argument — brands and agencies are increasingly framing human-led creative judgment as a premium service in response to AI commoditization of content. SMBs investing in marketing or content shouldn’t act on this directly, but it’s worth being aware of as a framing trend showing up in agency and creative-services pitches.

Calls to Action:

🔹 Deprioritize — this is opinion/trend commentary with no actionable AI signal for most SMB leaders

🔹 Note for context: expect more marketing/agency pitches positioning “human taste” as a premium differentiator from AI-generated content going forward

Summary by ReadAboutAI.com

https://www.fastcompany.com/91562674/winning-in-the-era-of-taste-and-talent-taste-marketing: June 30, 2026

Inside AI’s $5 Trillion Bet on Teaching Machines Taste

Source: Fast Company, 06-26-2026 | By Elizabeth Segran

TL;DR: AI shopping agents can already handle spec-driven purchases like appliances and tires, but the harder, more lucrative problem — understanding brand affinity and personal style — remains largely unsolved, and whoever solves it first stands to capture a market McKinsey estimates at up to $5 trillion globally.

Executive Summary: The author’s first-person test of ChatGPT for fashion shopping illustrates a broader industry gap: AI assistants are reasonably capable with “spec-heavy” purchases (electronics, appliances, tires) but struggle badly with taste-driven categories like fashion, where brand affinity and aesthetic sensibility matter more than specs. 2% of all ChatGPT queries — roughly 50 million daily — already involve shopping, and McKinsey projects AI assistants could enable up to $1 trillion in US shopping and $5 trillion globally by 2030.

The infrastructure for “agentic commerce” is actively being built: OpenAI/Stripe’s Agentic Commerce Protocol and Google/Shopify’s Universal Commerce Protocol aim to give AI agents access to inventory, pricing, and checkout systems that LLMs can’t naturally access on their own. Checkout remains the hardest unsolved piece — OpenAI walked back its Instant Checkout feature with Shopify six months after launch due to technical issues and weak user response, while Google has had more success embedding checkout into Gemini and AI-mode search.

A forward-looking claim worth flagging as speculation, not demonstrated fact: industry sources (including OpenAI and Google commerce leads) say these problems will largely resolve “by the end of this year” — a forecast from interested parties, not an independent assessment. Separately, the piece argues Google’s Gemini has a structural data advantagefor solving the “taste” problem via its new Personal Intelligence feature, which can draw on Gmail, Drive, Photos, and YouTube history — access that ChatGPT and Claude don’t have absent explicit user sharing.

Relevance for Business: For SMB retailers and brands, the actionable implication is about AI legibility: as agentic shopping matures, brands will increasingly need to make their value proposition explicit and machine-readable (not just visually compelling to humans) — through detailed brand language deployed across the web — to be correctly surfaced and recommended by AI shopping agents. This is an emerging SEO-adjacent discipline with no settled standard yet.

Calls to Action:

🔹 Monitor agentic commerce protocol developments (OpenAI/Stripe, Google/Shopify) — standards are still forming

🔹 Test cautiously: if you sell spec-heavy products (electronics, hardware, appliances), AI shopping assistants may already be a meaningful discovery channel worth optimizing for

🔹 Prepare brand language and product descriptions for machine readability, not just human appeal, as “AI legibility” becomes a competitive factor

🔹 Watch Google’s Personal Intelligence rollout — if it scales, Gemini could become disproportionately influential in consumer purchase recommendations

🔹 Deprioritize acting on checkout-integration specifics for now — the technology (Instant Checkout, etc.) is still unstable

Summary by ReadAboutAI.com

https://www.fastcompany.com/91549049/agentic-commerce-ai-human-taste: June 30, 2026

SpaceX’s IPO Windfall vs. Blue Origin’s Worthless Options: A Cautionary Tale in Equity Design

Business Insider — June 26, 2026

TL;DR: SpaceX’s record IPO turned even early hourly workers into millionaires, while Blue Origin’s stricter, IPO-or-bust equity structure left former employees with nothing — a structural lesson now directly relevant to how major AI labs design retention pay.

Executive Summary Former Blue Origin employees told Business Insider their stock options are effectively worthless, because Bezos’s company tied payouts exclusively to a liquidity event (IPO or sale) with a 10-year expiration — and Bezos never took the company public or sold it. SpaceX, by contrast, let employees cash out periodically through private liquidity events held roughly twice a year, independent of any IPO. One example cited: an employee with 9,000 SpaceX options granted in 2016 would be worth over $1.3 million today; the Blue Origin equivalent would be worth nothing. Bezos reportedly warned employees as early as 2016 that the options were closer to a long-shot bet than guaranteed wealth.

The detail most relevant to AI-watchers: the article notes that OpenAI, Anthropic, and Stripe reportedly use SpaceX’s model — allowing current and former employees to sell shares in periodic private liquidity events rather than waiting on an eventual IPO.

What’s fact vs. framing: The core structural comparison is documented (internal equity plan terms). The anecdotes from former employees are individual accounts, not verified financial outcomes; treat dollar figures as illustrative, not audited.

Relevance for Business Not directly about AI products, but relevant to AI talent strategy: this is the retention model several frontier AI labs are using to keep researchers from jumping ship before an eventual exit. If you’re trying to recruit against — or retain talent who might be tempted by — these labs, understand that liquidity-event access (not just headline compensation) is a real differentiator. It’s also a general governance lesson for any business issuing equity: vague or restrictive liquidity terms can quietly become a retention liability years later.

Calls to Action

🔹 Ignore for now — limited direct relevance unless your business issues equity compensation or competes for talent against AI labs.

🔹 Monitor — equity/retention practices at AI labs you compete with for talent, since liquidity terms matter as much as headline pay.

🔹 Revisit later — if your own company uses options-based compensation, this is a reasonable case study to bring to a future equity-plan review.

Summary by ReadAboutAI.com

https://www.businessinsider.com/spacex-employees-rich-ipo-blue-origin-workers-equity-2026-6: June 30, 2026

Anthropic Salaries Revealed: What H-1B Filings Show About AI Talent Pay

Business Insider — June 26, 2026

TL;DR: Federal visa filings show some Anthropic technical staff pulling in base salaries above $1.3 million — before equity or bonus — a window into just how aggressively AI labs are bidding for talent as they prepare for possible IPOs.

Executive Summary H-1B sponsorship filings (not full payroll data) show Anthropic’s “Member of Technical Staff” title — a broad catch-all spanning researchers to executives — paying anywhere from roughly $134,000 to $1.38 million in base salary alone. Two filings exceeded $1.1 million. The numbers exclude equity, which likely makes up a large share of total compensation given Anthropic’s $965 billion valuation as of this May. Anthropic sponsored roughly 80 H-1B roles in the first two quarters of fiscal 2026, even as some larger tech firms pulled back on visa applications — a sign of how concentrated the AI talent war has become among Anthropic, OpenAI, Nvidia, Meta, and Google. One data point worth treating as directional, not definitive: retention researcher SignalFire reported Anthropic holding onto staff at a higher rate than rival labs.

What’s fact vs. framing: The salary figures are documented in federal filings — that part is solid. What’s not knowable from this data is what these roles actually do, since the job title is so broadly applied. Anthropic declined to comment.

Relevance for Business This isn’t really about Anthropic’s payroll — it’s a labor-market signal. If you compete for any AI-adjacent talent (ML engineers, data scientists, even technical PMs), these numbers reset the ceiling candidates will benchmark against, even at companies far smaller than Anthropic. It’s also a vendor-stability signal: a company that can pay and retain talent at this level is less likely to suffer the execution gaps that come from staff churn — relevant if you’re evaluating Claude or other Anthropic products as a long-term platform bet.

Calls to Action

🔹 Monitor — track AI labor-market compensation trends if you’re hiring any technical AI roles; expect candidate expectations to be shaped by these headline numbers even at SMB scale.

🔹 Ignore for now — the specific salary figures themselves have no direct operational relevance unless you’re recruiting from these labs.

🔹 Monitor — Anthropic’s retention strength as one (imperfect) input into vendor-dependency risk assessment.

Summary by ReadAboutAI.com

https://www.businessinsider.com/anthropic-salaries-revealed-how-much-technical-staff-make-in-2026-2026-6: June 30, 2026

AMERICANS AND AI 2026: CHATBOTS, SMART DEVICES AND VIEWS ON IMPACT

PEW RESEARCH CENTER, JUNE 17, 2026

TL;DR: Chatbot use among U.S. adults has nearly doubled since 2024 — but majorities still believe AI is moving too fast, will erode their data security, and that neither government nor industry can manage it responsibly.

Executive Summary: This is primary survey research (5,119 U.S. adults, Feb. 2026) — the most authoritative source-type in this batch; treat findings as reported fact, not framing. Chatbot use jumped from 33% to 49% of adults since 2024, with about a quarter using chatbots daily. ChatGPT dominates at 44% usage, far ahead of Gemini (24%), Copilot (17%), Meta AI (14%), Grok (8%), Claude (6%), and Character.ai (3%). Primary uses are practical — search/information (42%) and work tasks (38% of employed adults) — while only 10% use chatbots for emotional support and fewer for companionship. Users report chatbots help more than hurt productivity, knowledge, and creativity, with minimal reported effect on happiness or relationships. Despite rising adoption, sentiment remains broadly negative: 63% think AI is advancing too quickly (vs. 2% too slowly), 71% expect it to make their personal data less secure, 67% have little confidence in government regulation (up from 62% in 2024), and ~60% distrust companies to develop AI responsibly. Notably, confidence in government regulation has flipped along party lines — Republican distrust dropped from 70% to 61% since 2024, while Democratic distrust rose sharply to 74%.

Relevance for Business:

- Mainstream adoption confirmed: Roughly half of U.S. adults now use AI chatbots — useful baseline data for any consumer-facing AI feature or messaging decision.

- Vendor concentration: ChatGPT’s commanding lead (44%) vs. smaller players like Claude (6%) is a concrete data point for platform-risk and negotiating-leverage assessments.

- Trust constraint on messaging: Majority skepticism about data security and regulatory oversight means AI features should be marketed with reassurance, not overconfidence.

- Productivity case data: The finding that users report net-positive productivity/creativity effects is useful supporting evidence for internal AI-adoption business cases.

Calls to Action:

🔹 Act now: Use the productivity/creativity benefit data as supporting evidence in internal AI-adoption business cases

🔹 Monitor: Vendor market-share shifts (especially smaller players like Claude) when evaluating platform risk

🔹 Prepare policy: Build customer messaging that acknowledges majority skepticism about AI’s pace and data security

🔹 Revisit later: Partisan regulatory-confidence shifts once trends stabilize

Summary by ReadAboutAI.com

https://www.pewresearch.org/internet/2026/06/17/americans-and-ai-2026-chatbots-smart-devices-and-views-on-impact/: June 30, 2026

AI IS WRITING ALMOST ALL STARTUP CODE. THAT’S CREATING A NEW PROBLEM.

BUSINESS INSIDER, JUNE 26, 2026

TL;DR: A Business Insider survey of startup founders finds AI — overwhelmingly Anthropic’s Claude Code — now writes nearly all code at many early-stage companies, but speed gains are increasingly offset by a “cleanup tax” of fixing low-quality, AI-generated output.

Executive Summary: This is an informal survey of 24+ founders/VCs — directional industry sentiment, not a rigorous study. Multiple founders report AI now writes “nearly 100%” of their code, a sharp rise from roughly a year ago. Anthropic’s Claude Code is described as the dominant tool of choice among those surveyed. Executives frame this as a structural shift in engineering work — from writing code to designing the context and guardrails AI operates within— with one founder predicting 80–90% of engineering tasks could be fully autonomous within a year. The flip side, per a cited Menlo Ventures report (an Anthropic investor), is a “Cleanup Tax”: time saved writing code is increasingly offset by quality-assurance work on fragile, unmaintainable output — described by one futurist as a coming “vibe coding” reckoning. Engineering “taste and judgment” is repeatedly cited as the remaining human differentiator.

Relevance for Business:

- Direct operational relevance for any SMB with software/dev needs: AI-coding tools can dramatically cut build time, but a real, currently underestimated maintenance/QA cost should be budgeted explicitly, not assumed away.

- Hiring/skills implication: the most valuable engineers going forward may be those skilled at directing and reviewing AI output rather than writing the most code themselves — relevant to hiring criteria and training priorities.

- Vendor signal: Claude Code’s reported dominance among startups surveyed is a useful anecdotal data point for tool selection, though it’s sentiment, not market-share data.

Calls to Action:

🔹 Test cautiously: Pilot AI-assisted coding with explicit QA/review checkpoints rather than assuming shipped code is production-ready

🔹 Prepare policy: Build “cleanup tax” time and cost explicitly into project estimates for AI-heavy development work

🔹 Monitor: Whether engineering hiring criteria should shift toward AI-direction and review skills

🔹 Revisit later: Forecasts of near-full engineering autonomy (80–90%) — currently a one-year projection from a single source, not demonstrated fact

Summary by ReadAboutAI.com

https://www.businessinsider.com/ai-writing-all-startup-code-thats-creating-a-new-problem-2026-6: June 30, 2026

Ford Says AI Alone Couldn’t Fix Its Quality Problems. It Needed to Rehire Veteran Engineers.

Business Insider, June 25, 2026

TL;DR: Ford credits its biggest quality turnaround in years to pairing AI tools with hundreds of rehired veteran engineers — a direct admission that automated quality systems underperformed when fed incomplete institutional knowledge, and a cautionary data point for any leader assuming AI can substitute for experienced staff rather than depend on them.

Executive Summary Ford was named the top mass-market brand (and second overall, behind Porsche) in JD Power’s latest initial-quality study, narrowly beating Lexus — a sharp reversal from three years ago, when it ranked 15th of 25 automakers. Executives attributed the turnaround partly to AI-enhanced quality tools, but offered a notably candid caveat: AI alone wasn’t sufficient. A VP of vehicle hardware engineering said the company had assumed that feeding design requirements into AI systems would automatically produce quality outcomes — and that assumption proved wrong, in part because Ford hadn’t adequately preserved the knowledge of experienced engineers who had since left the company.

The fix involved hiring, promoting, or bringing back roughly 350 veteran technical specialists — more than doubling that population since the 2023 quality reset began — to mentor junior staff, lead mandatory design reviews, and catch failure points before parts reach the production floor. Ford also restructured around an “industrial systems team” meant to break down the organizational silos (design, manufacturing, software, hardware) where it says quality problems most often originated, moving away from a reactive “find and fix” model. Important caveat: the JD Power award measures initial quality in new vehicles, not long-term durability — and Ford has still issued 51 recalls in 2026 so far (after a record 152 in 2025), with executives describing those as a “lagging indicator” tied to older vehicle platforms rather than current performance.

Relevance for Business This is a useful counterweight to AI-replaces-expertise narratives. Ford’s experience suggests AI tools are only as reliable as the institutional knowledge and data quality behind them — a direct garbage-in-garbage-out risk for any organization automating quality, compliance, or technical review processes without first securing the tacit knowledge of experienced staff. It also illustrates a labor implication worth flagging: the fix wasn’t “less AI,” it was AI plus reinvested human expertise, including rehiring people the company had let go. For SMBs running lean technical teams, this is a signal to be cautious about treating AI deployment as a reason to thin out senior technical staff.

Calls to Action

🔹 Assign internal review: audit whether your organization has documented the tacit knowledge of senior technical/operational staff before any AI automation initiative — Ford’s failure mode was an information gap, not a model failure.

🔹 Monitor: track whether your own AI-driven quality, compliance, or review tools are producing results consistent with experienced human judgment, or are quietly degrading over time as institutional knowledge erodes.

🔹 Prepare policy: build retention or knowledge-transfer plans for senior staff before assuming AI tools can absorb their function.

🔹 Test cautiously: if using AI for review/QA-type tasks, pair it with human oversight at organizational “boundary points” (e.g., where teams or systems hand off work) — Ford specifically flagged these as failure-prone zones.

🔹 Revisit later: the JD Power result measures new-vehicle quality, not durability — treat this as an early positive signal, not full proof the underlying recall problem is solved.

Summary by ReadAboutAI.com

https://www.businessinsider.com/ford-ai-hiring-veteran-engineers-2026-6: June 30, 2026

The Next Big Breakthrough Will Be AIs Learning on the Job

Dwarkesh Patel, June 26, 2026

Source type: opinion/research essay (author’s argument), not reported news — claims below are the author’s analysis and industry framing, not established fact.

TL;DR: Leading AI labs are betting that training models to complete millions of verifiable tasks will eventually produce general intelligence — but the author argues this approach hits a wall outside narrow, “grindable” domains like coding, and that the real unlock will be giving models a way to learn from real-world deployment rather than discarding that experience after each session.

Executive Summary: The essay lays out the current dominant research bet at major labs: training AI on millions of verifiable tasks across reinforcement-learning (RL) environments, on the theory that this builds general problem-solving skill. The author’s central argument is that this works well in domains that are not just verifiable but “grindable” — meaning thousands of identical scenarios can be cheaply and repeatedly simulated (coding is the clearest example). Domains like building a business, practicing law, or political strategy can’t be cheaply simulated, which the author argues explains why AI progress in less repeatable domains (e.g., computer-use automation) has been surprisingly slow despite being theoretically verifiable.

The piece’s more significant claim for business audiences: most AI lab compute spent on serving users today is, in the author’s framing, “wasted” — useful in the moment, but not feeding back into model improvement, because labs currently have no efficient way to convert real-world session experience into permanent model upgrades. The author discusses early technical approaches (e.g., “on-policy self-distillation”) aimed at solving this, alongside a more speculative idea — models running internal simulations to rehearse skills — that the author explicitly labels speculative, not demonstrated. The piece also cites a comment attributed to Anthropic’s Dario Amodei suggesting that model performance can degrade when training and deployment context lengths diverge, used by the author as evidence that current training approaches may not generalize as fully as labs are hoping. The author projects that by around 2027, AI systems could work alongside users for extended periods (a week or more) and have that accumulated experience folded back into the model — a meaningfully different paradigm from today’s training-then-deployment model, but this is the author’s forecast, not a confirmed lab roadmap.

Relevance for Business: This essay matters less for what’s available today and more for what to expect from your AI vendors’ roadmaps over the next 12–24 months. If labs do crack continual learning, AI tools could begin meaningfully improving based on your organization’s specific usage patterns — a potential competitive advantage for early, heavy adopters, but also a new data governance question: what happens to your organization’s usage data if it’s used to improve a vendor’s model going forward. It’s also a useful caution against assuming current AI limitations (e.g., weak performance on long, ambiguous, real-world tasks) are permanent — labs are actively targeting this gap, even if the timeline and method remain unproven.

Calls to Action:

🔹 Monitor vendor announcements around “continual learning,” “on-the-job learning,” or session-based model improvement — this is a stated lab priority, not yet a shipped capability.

🔹 Flag for governance review any AI vendor contract language about whether your usage/session data can be used to retrain or improve the underlying model.

🔹 Avoid overreacting to this piece as a near-term capability change — treat it as informed speculation about lab research direction, not a product announcement.

🔹 Revisit internal assumptions about AI limitations in long-horizon, ambiguous tasks (e.g., strategic or judgment-heavy work) periodically, as this is an area labs are explicitly targeting.

🔹 Assign internal owner (IT/AI lead) to track this space if your business is evaluating long-term AI vendor commitments tied to capability roadmaps.

Summary by ReadAboutAI.com

https://www.dwarkesh.com/p/the-next-paradigm: June 30, 2026

What Rebuilding AlphaGo Reveals About the Falling Cost of Frontier AI Research “BUILDING ALPHAGO FROM SCRATCH”

DWARKESH PATEL × ERIC JANG

Note: this is a technical research interview, not a business-news piece — I’ve pulled out the parts with genuine executive relevance and left the deep mechanics of Monte Carlo tree search aside, per the lighter-touch handling appropriate for highly technical transcripts.

Dwarkesh Podcast, May 15, 2026 — Eric Jang interviewed by Dwarkesh Patel

TL;DR: A solo researcher rebuilding AlphaGo on sabbatical illustrates a broader and more business-relevant trend than the Go game itself: work that once required a full DeepMind research team and millions of dollars in compute can now be replicated for a few thousand dollars, thanks to LLM-assisted coding — a signal that the cost of reproducing (though not necessarily originating) frontier AI capability is collapsing.

Executive Summary

The conversation is a deep technical walkthrough of how AlphaGo works (search, value/policy networks, self-play), which is not directly business-relevant and is excluded from this summary. What is relevant is the framing around how the project got built at all: Jang notes that LLM coding tools have reduced what once took a research team millions of dollars to a few-thousand-dollar effort, a claim consistent with broader industry commentary on AI-assisted software development but specific to research replication rather than novel discovery.

The discussion also surfaces a useful, less hyped distinction for evaluating AI-research-automation claims generally: LLMs are reported to be already capable of automating routine execution work — implementing experiments, running them, tuning hyperparameters — but still struggle with the higher-judgment work of choosing which research question to pursue next or recognizing when an approach has hit a dead end. This is a useful corrective for executives encountering broader claims about AI automating R&D wholesale: the evidence here points to automation of execution, not judgment, at least for now.

One framing note: the source mentions Anthropic’s Claude favorably (citing it producing a reasonable code implementation during the project). We flag this as a single anecdotal mention from one practitioner, not independent validation of comparative model performance.

Relevance for Business

- Lower barrier to in-house AI prototyping: If reproducing established techniques is now within reach of a single skilled engineer with modest compute spend, smaller firms may have more realistic options for building custom AI tools internally rather than only buying vendor solutions — though this applies to known, well-documentedtechniques, not novel research.

- R&D automation is uneven, not uniform: Treat any vendor or industry claim of “AI automating research” with the same distinction surfaced here — ask specifically whether the claim is about automating execution (a real, demonstrated capability) or judgment/strategy (still largely human-driven, per this account).

- Talent cost structure may be shifting: If routine research-engineering tasks are increasingly automatable, the relative value of senior judgment in technical roles may be rising even as junior execution-heavy roles face more pressure — a workforce-planning consideration for AI-adjacent hiring.

Calls to Action

🔹 Monitor — Track whether the “execution-yes, judgment-no” pattern described here holds up as AI coding and research tools mature; this is a useful lens for evaluating future AI-research-automation claims.

🔹 Investigate further— If your business is evaluating build-vs-buy on AI tooling, the falling cost of reproducing known techniques may change that calculus; worth a scoped internal assessment rather than assumption.

🔹 Deprioritize for most readers — The technical content (MCTS, value/policy networks) is interesting context but not actionable for non-technical SMB leadership.

🔹 Treat compute-cost claims as anecdotal — “A few thousand dollars” is one practitioner’s account, not a benchmarked industry figure; useful as a directional signal, not a budgeting input.

Summary by ReadAboutAI.com

https://www.dwarkesh.com/p/eric-jang: June 30, 2026

Japan’s Nikkei Hits a Streak Not Seen Since 1989 — AI Demand Is Only Part of the Story

MarketWatch — June 25, 2026

TL;DR: Japan’s Nikkei 225 is up nearly 44% this year, outpacing the S&P 500 by a wide margin, driven by a mix of corporate reform, exit from deflation, and surging demand for Japanese AI-hardware suppliers like Kioxia and Tokyo Electron.

Executive Summary: Japan’s stock market just posted its longest streak of consecutive record highs since 1989, with the Nikkei 225 up 43.8% year-to-date versus the S&P 500’s 7.5%. The rally isn’t a single-cause story: strategists point to Japan’s new prime minister’s pro-business stance, a structural shift out of decades of deflation that’s giving companies new pricing power, and a wave of investor demand for AI-hardware suppliers.

The AI angle is concentrated, not broad: memory-chip maker Kioxia is up roughly 895% this year and equipment maker Tokyo Electron is up 119.5% — both direct beneficiaries of AI infrastructure spending happening largely in the U.S. This mirrors a pattern seen in South Korea, where AI-driven gains are concentrated in just two firms (SK Hynix, Samsung). The distinction matters: Japan’s broader market gains are not solely an AI story — reform and macro factors are doing real work — but the AI-linked names are producing extreme, possibly unsustainable, outlier returns.

A secondary factor worth flagging for monitoring: yen volatility has drawn U.S. Treasury attention, raising the possibility of currency intervention — a wildcard that strategists say isn’t core to the investment case but could affect timing.

Relevance for Business: For SMB leaders with international exposure (supply chain, investment, or partnerships touching Japan), this signals a structurally improving Japanese business environment, not just an AI bubble proxy. The component to watch closely is concentration risk in AI-hardware names — those triple-digit-percent gains in single equipment suppliers are the kind of move that historically corrects sharply. Currency policy risk is also relevant for any business with yen-denominated costs or revenue.

Calls to Action:

🔹 Monitor — Watch for any signal of Bank of Japan or U.S. Treasury currency intervention, which could move yen-denominated costs quickly.

🔹 Investigate further — If your business has Japan-based suppliers or partners, this reform-driven pricing power shift may open new negotiating dynamics.

🔹 Ignore for now — The extreme AI-hardware stock gains (Kioxia, Tokyo Electron) are a public-markets phenomenon with no direct operational relevance for most SMBs unless you hold these securities.

🔹 Revisit later — Reassess after Q3 if the Nikkei’s record streak continues or reverses; durability of the rally is still an open question among strategists themselves.

Summary by ReadAboutAI.com

https://www.wsj.com/wsjplus/dashboard/articles/japanese-stocks-are-on-fire-heres-whats-driving-the-hot-streak-526a6914: June 30, 2026

The Magnificent Seven Trade Is Cracking — $3 Trillion Lost in a Month

Barron’s — June 26, 2026

TL;DR: The seven megacap tech stocks that dominated markets since 2023 have shed roughly $3 trillion in value this month, as AI-infrastructure suppliers and chipmakers outside the group — not the Mag Seven themselves — are now driving market gains.

Executive Summary: The Magnificent Seven trade — long the market’s most crowded position — is having its worst month on record, with the Roundhill Mag Seven ETF down 13% in June while the rest of the S&P 500 is up 2.6%. The reasons differ by company: heavy AI-infrastructure capital spending (Amazon, Meta, Microsoft, Alphabet), intensifying chip competition (Nvidia), rising input costs (Apple’s memory-price exposure), and ordinary volatility (Tesla).

The more structurally important shift: market leadership has moved downstream to companies that supply the Mag Seven rather than the Mag Seven itself. Memory-chip maker Micron now has a market cap approaching Meta’s, and equipment/chip suppliers Applied Materials and Broadcom have become among the most “crowded” hedge fund positions — alongside Nvidia. This suggests investor enthusiasm for AI hasn’t cooled, but where that enthusiasm is concentrated has shifted toward hardware suppliers and away from the platform companies themselves.

One real silver lining flagged by strategists: the credit markets still see the Mag Seven as highly reliable, with the AI cloud providers issuing large volumes of debt to finance chip and data-center buildouts — suggesting bond investors aren’t pricing in the same risk equity investors currently are.

Relevance for Business: This is a useful corrective for any SMB leader treating “the Mag Seven” as a single proxy for AI-market health — the underlying picture is now fragmented by company-specific exposure (capex risk, chip competition, input costs), not a unified AI growth story. It’s also a signal that capital intensity is the dominant theme for the largest AI spenders: heavy debt issuance to fund infrastructure is becoming normalized at the top of the market, which has knock-on implications for chip/hardware supply and pricing further down the value chain.

Calls to Action:

🔹 Monitor — Track whether the rotation toward chip/equipment suppliers (Micron, Applied Materials, Broadcom) continues; it’s a leading indicator of where AI infrastructure spending is actually flowing.

🔹 Act now (if applicable) — If your business has cost exposure to memory/chip pricing (e.g., hardware-dependent operations), factor in continued volatility from this supplier-side demand surge.

🔹 Deprioritize — Treating “Mag Seven performance” as a single AI-market health indicator is no longer reliable; don’t use it as a proxy in strategic planning.

🔹 Revisit later — Reassess after Q3 earnings, which will clarify whether the capex-heavy names’ spending is translating into revenue or just margin pressure.

Summary by ReadAboutAI.com

https://www.wsj.com/wsjplus/dashboard/articles/mag-7-etf-roundhill-big-tech-stocks-a2eca38e: June 30, 2026

Jeff Bezos-Backed Slate Reveals EV Pickup’s Price

Business Insider — June 24, 2026

AI-Leader Connection: Backed by Amazon founder Jeff Bezos.

What Happened: Slate priced its bare-bones electric pickup at $24,950 (SUV variant at $29,950), positioning it as the “most affordable truck in America.” The strategy leans on minimal standard features (manual windows, no touchscreen) paired with 200+ optional accessories, Build-A-Bear style. The launch comes after the federal EV tax credit expired and amid a broader EV sales slump, with over 180,000 refundable reservations placed so far — a figure the source notes has historically overstated real demand.

Why AI-Readers Should Care: No direct AI relevance — this is a consumer EV story included for visibility into one of Bezos’s other bets, separate from his AI/cloud interests via Amazon.

TL;DR: Bezos-backed startup Slate priced its bare-bones electric pickup at $24,950, betting that stripped-down, customizable vehicles can find buyers in a price-sensitive EV market just as federal tax credits have disappeared — a notable consumer/EV story, but not an AI development.

Executive Summary Slate’s base two-seat electric pickup starts at $24,950 (SUV variant at $29,950), pitched as the “most affordable truck in America.” The strategy: minimal standard features (manual windows, no touchscreen, no stereo) with 200+ optional accessories for later customization — an explicit “Build-A-Bear” approach to vehicle ownership. Deliveries are expected by end of 2026.

The timing is a genuine risk factor: Slate originally targeted sub-$20,000 pricing assuming the federal $7,500 EV tax credit, which ended in September, and EV sales have slumped since. The company also now faces more competition at the low end (Rivian R2, Toyota C-HR, Lucid’s Cosmos). More than 180,000 people have placed refundable $50 reservations — a figure the article explicitly cautions is a weak demand signal, citing the Ford F-150 Lightning’s ~200,000 reservations followed by discontinuation after four years.

This is not an AI development. There is no AI angle in this story; it’s a consumer EV/manufacturing piece relevant only insofar as it involves a high-profile tech investor.

Relevance for Business Limited direct relevance to AI-focused SMB strategy. If relevant at all, it’s as a general business-model case study: a low-margin, accessory-driven revenue model in a market where reservation counts have historically overstated real demand — a useful cautionary pattern for any business relying on pre-order signals to validate a launch.

Calls to Action

🔹 Ignore for now — no direct AI or SMB-strategy relevance.

Summary by ReadAboutAI.com

https://www.businessinsider.com/slate-ev-pickup-starting-price-2026-6: June 30, 2026

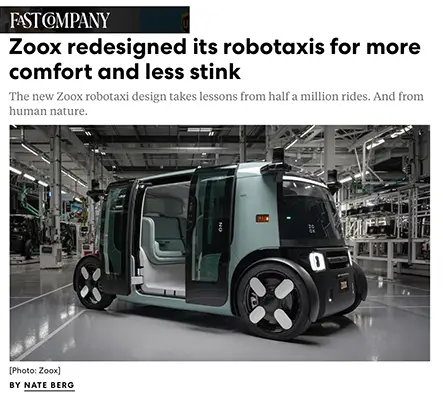

ZOOX REDESIGNED ITS ROBOTAXIS FOR MORE COMFORT (AND LESS STINK)

Fast Company — June 24, 2026

AI-Leader Connection: Amazon-owned autonomous vehicle unit.

What Happened: Zoox redesigned its robotaxi interior using data from roughly 500,000 rides in San Francisco and Las Vegas, focusing on more durable, easier-to-clean materials, improved seating, and brighter cabin lighting. The company frames the changes as an operational play — better materials mean less downtime and fewer part replacements for its fleet. The new version also includes an exterior interface module for emergency communication and is expected to launch later this year, with testing planned in Austin and Miami.